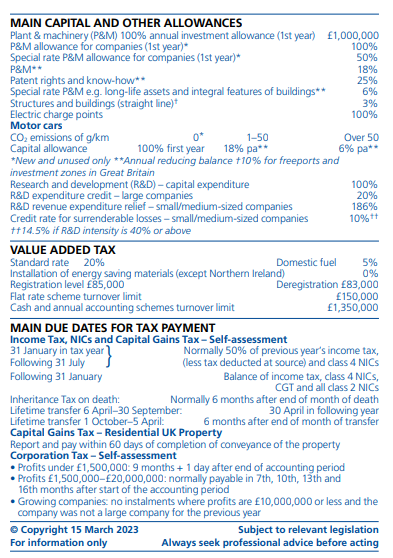

Current Tax Rates

We know all about taxes

Choose Bird Simpson & Co, Dundee for the latest information on the current tax rates and

tax advice.

Tax card

Call Bird Simpson & Co in Dundee on

01382 227 841 for current tax rates.

© 2024. The content on this website is owned by us and our licensors. Do not copy any content (including images) without our consent.